by Justin Deem, Vice President of Appraisal Operations

When applying for proper property insurance coverage, it’s important to have a complete and accurate property schedule. Why? A well-prepared schedule of information helps ensure accurate coverage and the best ratings possible. It speeds up the underwriting process and provides transparency for everyone involved in the process. Plus, you get peace of mind, knowing the cost and efforts to prepare an accurate schedule can lead to a reduction in premiums.

This blog post will walk you through common mistakes that we typically see on a property schedule and offer ways that you can check the completeness of your information to avoid pitfalls.

What is a Property Schedule?

It’s a comprehensive report of properties that an insured organization submits to an insurer. The detail for each schedule varies depending upon the policy requirements, as well as what types of properties you’re insuring. Ultimately, the report provides the amount for each property type (Property in the Open, Content Values, Machinery and Equipment, and Buildings) and outlines the total insurable value for each location.

Typically, when we see mistakes in property schedules, they fall into one the seven following categories:

- Outdated Buildings, Structures and Property Listings

- Treatment Plants Listed as a Single Line Item

- Inconsistent ISO and Construction Class

- Missing information and Incomplete Data

- Common Red Flag Inconsistencies

- Historical Structures: Confusion Between Replacement Costs and Reproduction Costs

- Inaccuracies in the Exclusion Amount

Let’s talk about each of these in more detail!

Outdated Building, Structure and Property Listings

Most mistakes we see in property schedules are inaccuracies in how the buildings, structures and overall property are recorded. Common discrepancies include:

- Buildings that were sold or demolished but were never removed from the schedule

- Buildings that needed to be added to the schedule, but weren’t

- Building additions that were constructed but never recorded

How It Affects Your Organization

When information changes but doesn’t get funneled to the appropriate staff for documentation, the accuracy of your data and your schedule is compromised. It causes newer buildings to be left without coverage, while you’re still paying to cover buildings that no longer exist.

Treatment Plants Listed as a Single Item

We see this often with water and wastewater treatment plant, where the whole plant is listed as a single line item. These structures tend to be valued by the treatment plant’s maximum capacity rather than broken out and valued individually on the schedule.

How It Affects Your Organization

The problem with treating a plant as one item is that each building at the plant is built for a specific process, and the function and cost of each structure varies significantly. The depths and heights for these structures can also have a significant impact on the cost. So listing a blanket amount for a treatment plant will not give you an accurate replacement cost in the event of an individual loss. It’s much better to break each structure out separately.

Inconsistent ISO and Construction Class

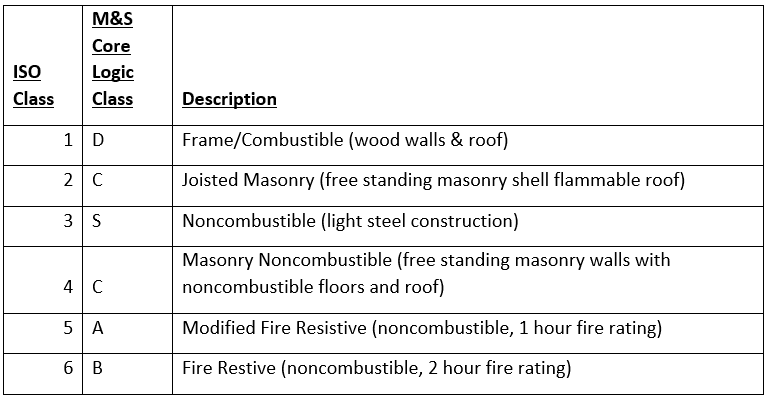

One of the primary goals of underwriting for property insurance is determining risk of fire. Most schedules include the Commercial Fire Rating Schedule, as well as the Marshall and Swift (M&S) Core Logic Construction class. Assigning the proper construction classes helps the underwriter understand the construction type and rate the risk more accurately. The Commercial Fire Rating Schedule is broken down into the classes listed below.

The ISO Class and M&S class must coincide with one another. For example, an ISO Class 3 must always have an M&S class of S.

To check that yours align, sort or filter your Schedule of Values, first by ISO and then by M&S class. A building with an ISO Class of 1 and an M&S class of B, for example, should draw some concern.

Why? The ISO class of 1 suggests the building has a combustible frame, while the M&S class B suggests it is fire resistive. Since these two things cannot be true at the same time, a discrepancy like this would merit further investigation.

How It Affects Your Organization

These inconsistencies mean underwriters are unable to assess your risk accurately. And because of this, you may end up with a “worst case scenario” risk rating, raising your insurance premiums

Missing Information and Incomplete Data

There are many reasons an organization might be missing data. Often, it’s simply because policy holders are uninformed about both the requirements and the impact that thorough data collection can have on premiums.

Within the last 10-15 years, significant wind and seismic events have prompted changes to insurance reporting, particularly with data models and the data they collect. Not long ago, the only data being collected was primary Construction Occupancy Protection Exposure (COPE) data. Now, as the models continue to evolve, new areas for data collection emerge and many organizations haven’t made the shift to filling in these gaps.

Catastrophe modeling, AKA “CAT modeling,” for example, has joined the primary data category. There are three primary CAT models used today:

- The AIR Worldwide model

- The Risk Management Solutions model

- The EQECAT model

Currently, the most common ones are RMS and AIR, however, all these models have similar data collection points because they focus on hurricane and earthquake information. This helps determine the amount of exposure, risk and loss expectancy for each property. Location particularly becomes a factor for these models.

How It Affects Your Organization

This new CAT modeling depends on data integrity, so incorrect or incomplete data for your property location, as well as hurricane and earthquake-related data points, increases the uncertainty of the model. That means, if you have missing or incomplete data on your property schedule in these areas, underwriters must assume the worst case, increasing your premiums. Investing in CAT modeling during the valuation process helps maximize the transparency of your property list, allowing you to leverage a better premium.

Common Red Flag Inconsistencies

While you’re following up on missing and incomplete data, there are some common red flags in property schedule data that you might also want to investigate, like:

- Are values for similar buildings all within a certain range or are there some questionable outliers?

- Do you notice any square footage listings that are exact and may have been rounded up?

- Are there “cookie cutter” buildings that report different attributes and information?

- Were addresses used to research flood zones? The only real accurate way to research flood zones is using GPS coordinates. At a school site that has multiple buildings with the same address, there could be multiple flood zones.

- Does every building on your property list have a physical address?

All of these questions can help reveal areas where data may not be correct.

How It Affects Your Organization

Consistent, quality property data helps improve your rating with underwriters. By eliminating trouble areas, you help strengthen your property schedule and your rates.

Historical Structures: Confusion Between Replacement Cost Versus Reproduction Cost

Another common issue we see on property schedules is confusion between replacement costs and reproduction costs related to historical properties.

A replacement cost is the cost to construct, at current prices as of the effective appraisal date, a substitute for the building being appraised, using modern materials and current standards, design, and layout.1

A reproduction cost is the estimated cost to construct, at current prices as of the effective date of the appraisal, an exact duplicate or replica of the building being appraised, using the same materials, construction standards, design, layout, and quality of workmanship and embodying all the deficiencies, superadequacies, and obsolescence of the subject building.1

For example, consider a house with plaster walls. A reproduction cost estimate requires estimating the cost to reconstruct the plaster walls exactly as they are. A replacement cost estimate, however, estimates the cost to put up sheet rock walls according to the current standard. The key difference is the type of improvement being considered. In the event of a risk incident, are you comfortable with insuring the building like a new building with modern materials, or an exact replica of the historical building? Citing this difference accurately on a property schedule can be critical for historical properties because remodeling or rebuilding historical structures often involves some serious attention to detail. Matching existing materials and preserving what already exists is challenging, requires research and the willingness to quest for the perfect resources.

I once appraised a historical post office. The detail was such that every single screw from the windows in the building needed to be wire brushed and refinished. Which goes to show that when you have a historical structure, you’re not just demoing and replacing; you are refinishing and reproducing.

How It Affects Your Organization

A historical building insured for replacement costs instead of reproduction costs means that a lot of the important structural details (those wire-brushed screws, for instance!) could be lost during rebuilding after a risk event; your insurance policy will not cover it. The loss of those details can mean losing an important piece of history — and that can affect your Historic Designation status and your property values, as well.

Inaccuracies in the Exclusion Amount

Exclusions generally consist of items that would be part of a structure’s original construction cost but are excluded from the replacement cost — typically because they either aren’t damaged or wouldn’t need to be replaced in the event of a catastrophe.

Some items that may be considered insurance exclusions include:

- Site preparation

- Basement excavation

- Below grade foundation walls

- Architects’ fees

- Interior foundation

- Piping below ground

- Debris removal / demolition

At Centurisk, our exclusions are calculated through a combination of years of corporate expertise and our proprietary software, RiskStar, and they’re based on the occupancy type and square footage of the building. Newer construction documents, such as the AIA document, break out the costs for these items.

With standard occupancies, we tend to see, on average, about 6% exclusion on the total replacement cost. So, let’s say an average office building has a replacement cost of $1 million dollars. The exclusion amount would be $60,000. Therefore, when we factor in the exclusion amount, the insurable value of that structure becomes $940,000. As you can see, the replacement costs on that office building could be reduced significantly, but often organizations don’t know to take advantage of the opportunity.

Other structures to consider when looking at exclusion amounts are water and wastewater treatment buildings. Many buildings located at these facilities are two to three stories below grade. If we consider that they have one story above grade and three below grade, more than 75% of the structure could be excluded from the replacement cost. (Also note: while most are constructed of reinforced concrete and may seem indestructible, they also have tons of water flowing through them at all depths. So it’s very important that the exclusions are listed and defined in your policy.)

Fortunately, most standard reports will show both values, the replacement cost and the replacement cost less exclusion amount. So you’ll always have that information right on hand, in order to make an informed decision on how you’d prefer to insure.

How It Affects Your Organization

Why pay to cover common exclusions? You can right-size your insurance coverage by taking the exclusions that make sense for your organization, improving your bottom line. We recommend, however, that you consult with your insurance broker first to clarify your exclusions, as well as to ensure you are properly covered

Greater Accuracy and Better Premiums Are Within Reach

Compiling a complete and accurate property schedule can be quite challenging. Especially if you are uninformed of your policies’ requirements and the impact that inaccurate and incomplete data can have on premiums. Consulting with your insurance broker or a valuation firm can help alleviate some of the stress. The cost to consult with a valuation firm can pay for itself with the savings in premiums over time. If you are unsure of the completeness of your property schedule, Centurisk is here to help. We are always willing to review and identify areas that may need improvement. We can help guide you through decisions as you work your way through the renewal process.

Sources:

- Appraisal Institute, The Dictionary of Real Estate Appraisal, 5th ed. (Chicago: Appraisal Institute, 2010).

About the Author

Justin Deem resides in Pittsburgh, PA, with his wife Gina and two children, Carter, six, and Landon, four. When he’s not acting as Operations Manager at Centurisk, he spends most of his free time with his family in quarantine! Seriously though, he spends most of his time outdoors in the yard working or enjoying family activities.