Imagine this scenario: A mid-sized city believes its community center is fully insured. Then a fire breaks out, consuming the building. When the smoke clears, the insurance policy, based on a $10 million replacement cost, falls $2 million short of the true rebuilding cost once debris removal, code updates, and urgent contractor premiums are included. That shortfall doesn’t just affect the city; it reverberates across the pool, straining reserves and creating difficult conversations.

This is the reality of underinsurance. And while some of it comes down to numbers, more often the problem is about operational practices, definitions, and misaligned expectations. The good news? With the right approach, underinsurance (or even the perception of underinsurance) can be significantly reduced, along with the stress and awkward moments that come with it.

Following are four key drivers that help public entities avoid underinsured property losses.

1. Address 100% of the Property Values Annually with Onsite Appraisals or Trends

At the foundation of every property insurance program lies one question: Are your insured values accurate?

An insurance appraisal program isn’t a one-and-done exercise. It’s a structured initiative to gather, establish, and maintain property data and values over time. Done right, it provides confidence to members, reinsurers, and brokers alike. Done poorly—or neglected altogether—it creates hidden exposures.

The most successful programs consistently include five elements:

- Comprehensive data collection. On-site inspections are non-negotiable. You can’t confidently confirm what you don’t see in person. At Centurisk, our appraisers typically discover that 10–25% of buildings owned by customer members aren’t listed on the current property schedule. When you start with a discrepancy that large, underinsurance becomes likely.

- Sound valuation methodology. Insurers, pools, pool members, and appraisers must align on the definitions of value to be used during an appraisal project and apply consistent, industry-standard methods. Disconnects in definitions lead to disconnects in expectations—resulting in awkward conversations and potential coverage gaps down the road.

- Ongoing updates. Values must be refreshed annually using region-specific trend factors, even for buildings not inspected that year. Building values are not static. Replacement, reproduction, and reconstruction costs shift with supply chains, inflation, labor, and material markets. Trending the values of properties that aren’t receiving on-site appraisals is essential.

- Reporting and transparency. Modern delivery methods (property risk-management platforms, digital reports) make it easier to share and verify data. Configurable reports in a centralized solution like RiskStar help identify inconsistencies across pool data and flag red-alerts for verification.

- Perpetuation planning. Spreadsheets alone won’t cut it. Property data needs to live in a secure, auditable system that captures history and approvals. With centralized electronic data collection and reporting, version-control issues fade. You can track and verify changes more easily and build confidence in the data you collect.

Bottom line: Accurate, current valuations protect against both under- and overinsurance, while strengthening credibility with reinsurers.

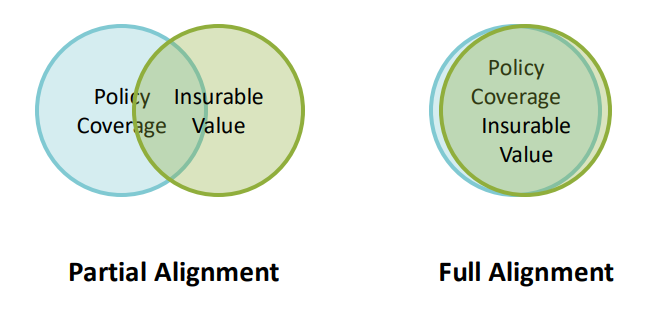

2. Align Definitions of Value with Policy Coverage

One of the most common sources of “phantom underinsurance” is a simple mismatch in definitions among the insurance policy, the pool, the pooling member, and the valuation firm.

Three valuation types commonly used in property insurance appraisals:

- Replacement Cost: Rebuilding with modern materials and standards.

- Reproduction Cost: Rebuilding an exact replica with the same kind of materials and processes (common for historical structures).

- Reconstruction Cost: The actual rebuilding cost at the site, including demolition, debris removal, code upgrades, and urgency factors.

Too often, these terms are used interchangeably, or not clarified at all, and that misalignment can lead to coverage gaps or inflated premiums.

Consider a school insured at a $10 million replacement cost. A true reconstruction, once demolition and compliance costs are factored in, could push the price tag closer to $12 million. That $2 million shortfall doesn’t just frustrate members; it directly impacts pool reserves.

Action step: Before engaging with an appraisal firm, review the definitions of value being applied. Values must align with policy coverage. When insurable values and policy definitions fully overlap, you minimize surprises at claim time.

3. Manage Post-Loss Expectations

Even when valuations are accurate and aligned, the appearance of underinsurance can still pop up post-loss if member expectations don’t match reality.

Members often assume their coverage will restore property to its former glory or even include new improvements. But policies don’t always fund upgrades, expansions, or amenities. When those expectations collide with actual coverage, disputes and frustrations arise.

Two case studies from Centurisk’s decades of experience:

- School consolidation. Two schools on the same site were destroyed by a tornado and later rebuilt as a single structure. Coverage, however, was based on two separate schools. During the same period, construction costs surged ~30% over two years and the pool did not apply recommended trend factors. The result: undervalued properties at the time of loss and significant shortfalls.

- Maintenance building. A $400,000 insured building was estimated at $600,000 to replace. A closer review showed the gap came from upgrades—spray insulation, interior partitions, and added square footage—implemented between on-site appraisals but never added to the property schedule. The perceived underinsurance was an added-scope issue, not a coverage failure.

Action step: Proactively document updated property attributes and set realistic coverage expectations before a loss. Centralized property management software helps you store photos, attributes, and history, so you can tell what changed and when, and separate valid claims from shifting scope.

4. Prioritize Member Education and Communication

The final driver ties everything together: ongoing education, communication, and scenario planning.

When members understand how valuations are determined, what policies cover, and how claims play out in practice, alignment improves across the pool and trust grows. Best practices we see working:

- Training and webinars. Partner with your appraisal firm to provide regular education tailored to current topics (e.g., construction trends). At Centurisk, we equip customers and their members with training, reference materials, and plain-language explainers. A unified message creates consistency and awareness across the pool.

- Loss-scenario modeling. Walk members through “what if” cases — like a school fire — to illustrate how demolition, debris removal, and today’s costs affect claims. This makes definitions of value concrete and practical.

- Proactive workflows. Encourage members to share construction documents for new builds. Reviewing costs up front prevents inflated values from being added to schedules.

- Collaborative policy reviews. Sit down with members annually to review appraisal reports alongside policy coverage and the statement of values, well before renewal season. Alignment early makes renewal smoother.

Takeaway: Member education isn’t just about preventing underinsurance; it’s about building relationships, sharing a consistent message, and earning trust.

Building Confidence, Reducing Risk

Preventing underinsured property losses isn’t just about math. It’s about establishing accurate valuations, aligning definitions, managing expectations, and investing in communication.

For pools, states, and public entities, getting this right improves data accuracy, protects financial stability, and builds long-term confidence with reinsurers and members alike.

Underinsurance is avoidable. With these four drivers in place, you can close gaps before a loss occurs—and give pool administrators, members, reinsurers, and brokers the peace of mind they deserve.

Want to explore how Centurisk can help your pool strengthen its appraisal program and prevent underinsurance? Contact us to start the conversation.

Note about this article:

Human-Led, AI-Assisted

This article was written by our team with modest assistance from AI tools.