Why Property Insurance Valuations Still Matter in a Soft Market

What Public Sector Risk Pools Should Do Before the Market Hardens Again

by Lauren Galietti, Vice President, Centurisk

After several challenging years in the property insurance market, conditions in 2026 are beginning to ease. Capacity is increasing, insurance carriers are competing more aggressively for business, and their pricing is stabilizing across many lines. Aon’s 2026 Property & Casualty Market Outlook believes that the more favorable conditions for insureds are being driven by improved insurer capital positions and intensified competition. For public sector risk pools and their members, that’s a welcome relief.

But soft markets carry a quiet risk that’s easy to overlook: when insurance becomes easier to buy, the less exciting work tends to slip down the priority list. In this case, “less exciting” could include: maintaining property data, updating valuations, and data auditing.

But letting these things slip is a mistake, because this is exactly the time when that work matters most.

What Goes Wrong When Valuations Fall Behind

A property insurance valuation determines the cost to rebuild or replace a structure after a loss. It’s what that property and all its features would actually cost to reconstruct. That figure is called Replacement Cost Value, or RCV.

For public entities, the properties in question include large community buildings like schools, courthouses, fire stations, water treatment plants, and public works facilities. These assets are often difficult and costly to replace, and because communities depend on them, they can’t just sit unoccupied during a coverage dispute.

When valuations aren’t updated regularly, the most common result is underinsurance: the property is insured for less than it would cost to rebuild. For example, a school insured for $20 million may carry a real replacement cost of $30 million after several years of construction inflation. Construction inflation is the rising cost of building materials and labor. That gap doesn’t become visible until there’s a loss, and by then, it’s too late to fix it cleanly.

As a result, a municipality might find itself in a budget crisis, face significant rebuilding delays, or become entangled in protracted disputes with carriers over coverage limits.

The Many Factors Leading to Today’s Misaligned Insured Values

The math has shifted considerably in recent years for several key valuation data points. Construction inflation has outpaced the rate at which many public entities have adjusted their insured values. Supply chain disruptions, labour shortages in the trades, increased material costs, and stricter building codes have all contributed to rising prices. This means when codes change, rebuilding often costs more than the original construction, regardless of what the policy might say.

During recent catastrophes, many public entities discovered that their insured values were 20 to 40 percent too low. At that scale, the gap between what a policy pays and the cost of reconstruction can turn a manageable claim into a genuine financial crisis.

The Underwriting Problem You May Not See Coming

Inaccurate property values don’t just affect claims; they can affect underwriting before any loss even occurs.

Insurers and reinsurers use property data to build catastrophe models that estimate the Probable Maximum Loss (PML), the largest expected loss from a major event such as a hurricane or earthquake. When property values are understated, those models underestimate the pool’s true exposure. That can affect pricing, coverage terms, and even the structure of a pool’s reinsurance program.

Reinsurance is the insurance that insurers and pools purchase to protect themselves against very large losses. If a pool’s property values are understated, the reinsurance program may have been sized for an exposure that no longer reflects reality. That’s a structural problem, and it’s one that typically only surfaces when it’s hardest to address.

Why a Soft Market is the Right Time to Fix All This

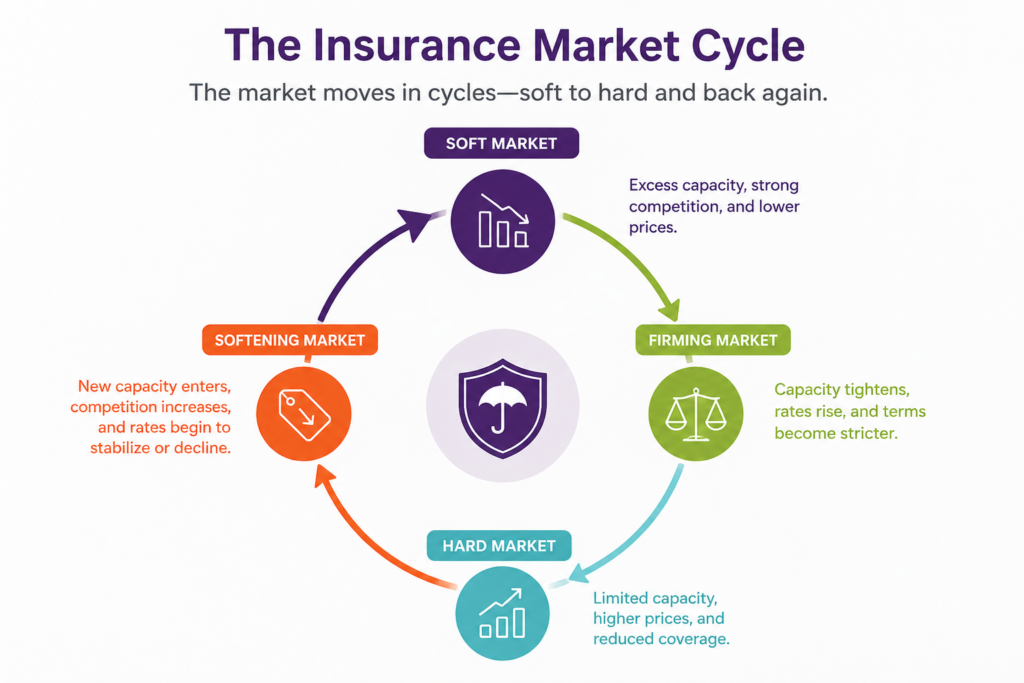

Soft markets are defined by increasing capacity, slower premium growth, broader insurance coverage terms, and carriers competing for business. Capacity, simply put, is how much risk insurers are willing to take on. So, when capital is strong and competition is high, capacity grows. Insurers can take on more insureds, and insured have better opportunities for the coverage they need at, potentially, better premiums.

But, keep in mind, soft markets are also temporary. Insurance cycles always shift, and the conditions that make a market soft, such as strong insurer capital and low catastrophe losses, can reverse quickly.

Many insurance professionals point to the mid-2010s as the last prolonged soft property market cycle before conditions hardened in the late 2010s and early 2020s.

Organizations that invest in property data and valuation projects during soft markets tend to be in a fundamentally stronger position later, when conditions harden. They’re not scrambling to explain their exposure to their carriers’ under-pricing pressure. They’re not discovering mid-renewal that their values are significantly off. And they’re presenting underwriters with the kind of clean, credible data that leads to better outcomes.

Centurisk customer, Kevin Meehan, knows the power of this soft market preparation. As Senior Vice President and Director of Trust Services for Preferred Governmental Insurance Trust, and Arrowhead Public Entity Vice President, he has seen the dynamic play out directly:

“One of the smartest things we did during the last soft market was to invest in getting our property valuations in order. When the market hardened later, we weren’t scrambling to explain our exposure data to carriers. It gave underwriters confidence in our program and helped us maintain stability when others were facing big surprises.”

What Good Property Data Looks Like

Modern insurers and reinsurers increasingly rely on detailed exposure information. This includes data like a property’s construction type, building age, roof condition, square footage, and occupancy. It can also include geographic hazard data like wind, flood, and wildfire risk. Risk pools that maintain accurate, up-to-date data at that level of detail consistently see better underwriting outcomes, because carriers and reinsurers can better evaluate what they’re actually taking on.

Better data leads to better underwriting confidence, which leads to better insurance outcomes. It may not sound like a complicated idea, but it requires consistent effort to maintain.

Which leads to a few questions worth asking in your organization:

When was the last full property appraisal conducted for member properties?

Have insured values been adjusted to reflect recent construction cost increases?

Are major renovations and additions being captured consistently as they occur?

Does the pool have exposure data that inspires confidence when you’re presenting risks to reinsurers?

If the answers are unclear, valuations deserve a closer look. But you’ll want to do it before the next renewal cycle, and well before the next hard market. Because your window of opportunity will close.

So many risk pools are investing in property data programs that combine on-site valuations, digital property inventories, and centralized exposure management. Together, this builds the kind of foundation that supports confident underwriting decisions at every stage of the market cycle.

At Centurisk, we work with public entities and risk pools to maintain accurate property data, improve valuation confidence, and support underwriting and reinsurance decisions with better exposure information. When property data is accurate, everyone in the risk financing chain — from members to reinsurers — can make better decisions.

Now is the Right Time

Insurance markets will continue to cycle between soft and hard conditions. That’s not going to change.

What doesn’t change is this: good underwriting starts with good data. For public sector risk pools, accurate property valuations are a foundation of responsible risk management. And when the market feels easiest, that’s the time to tackle the hard stuff and make sure everything is still accurate.

Note about this article:

This article was written from an AI-generated draft that our team expanded and fact-checked.

Sign Up

Subscribe for blog updates, educational videos, case studies and infographics.